Iván Hernández Dalas: Chinese robotics outlook for 2026 includes cobot growth, competitive pressure

Specs of the Unitree H2 humanoid robot, one of several being developed in China. Source: Unitree

Based on our data, Chinese industrial robot sales again in 2025 by roughly 10%. With other major markets comparatively weaker, China further cemented its top position in global robot sales. For 2026, we are cautiously optimistic and expect mid- to high-single-digit growth.

Sales of collaborative robots in China have outpaced the broader market over the past two years — and there are strong indications that this trend will continue. Key drivers include easier installation, high flexibility, relatively low energy consumption, and new applications, particularly in electric-vehicle manufacturing.

Intense price pressure — and the consolidation that comes with it — will persist. At the same time, we see both industrial robots and cobots trending toward more “intelligent” solutions as a means of differentiation, such as semi-autonomous welding.

After China’s industrial robot exports grew by an average of about 65% per year from 2022 to 2024, that momentum continued in 2025. While full-year 2025 figures are not yet available, export levels had already surpassed the prior year’s total by the end of the third quarter. We expect this trajectory to continue into 2026.

More Chinese capital flows into embodied AI

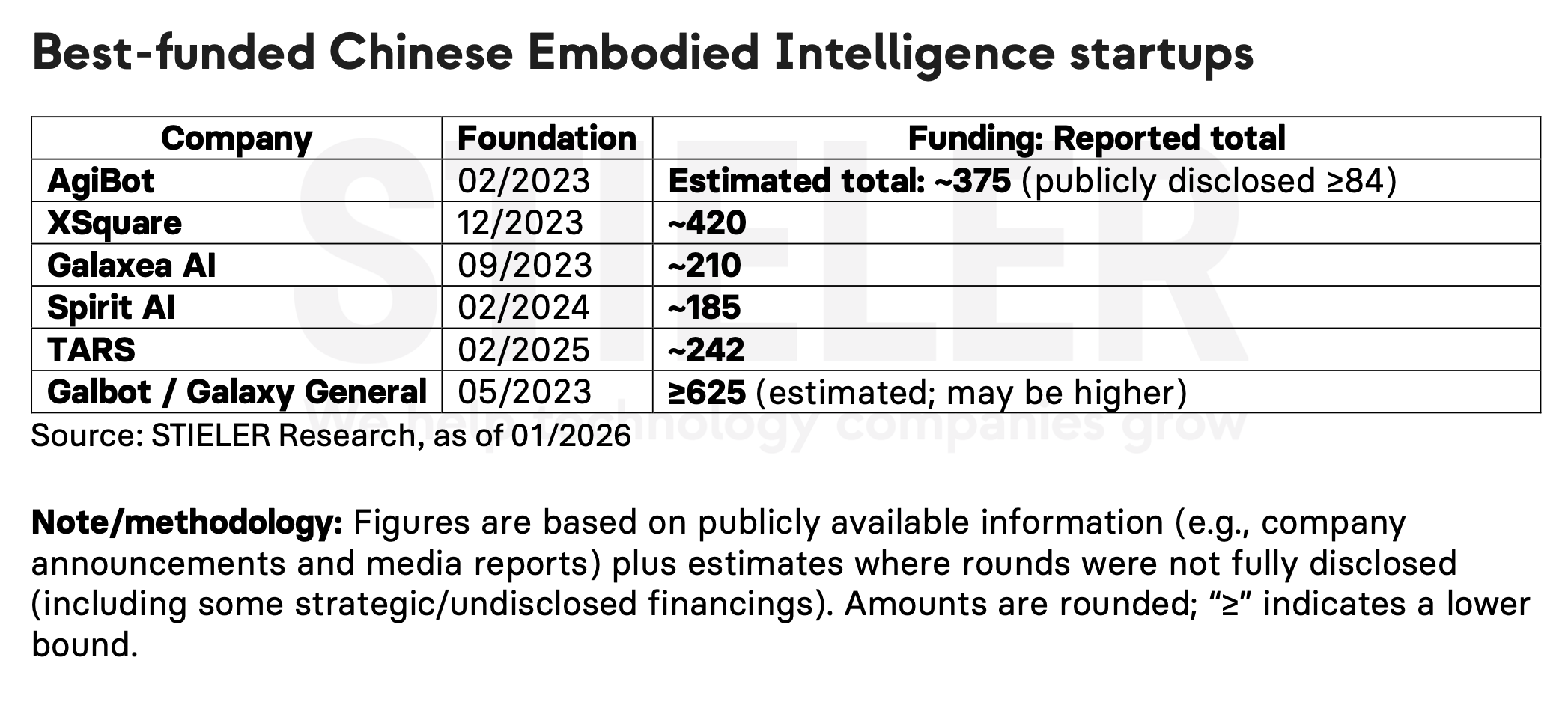

China is moving alongside to the U.S. the forefront of development in physical AI. By our estimates, investment in early-stage robotics companies in both the U.S. and China in 2025 was roughly five to six times higher than in Europe.

In China alone, we see at least five embodied AI companies that have each raised more than $210 million to date, and capital continues to flow aggressively into the space: On Jan. 12, X Square announced it had raised RMB 1 billion (about $140 million) in an A++ round led by ByteDance and HongShan Capital (formerly Sequoia China). Meituan and Alibaba had participated in earlier rounds. In just two years, X Square has raised more than $400 million.

X Square is pursuing what founder Wang Qian calls “an independent foundation model for embodied AI.” The core thesis: AI designed for the physical world requires different architectures than language models.

According to the company, its WALL‑A system not only processes visual inputs, but it can also “understand” causal physical relationships — enabling robots, for example, to infer hidden objects and autonomously correct errors without human intervention.

Many in the West have primarily been watching U.S. efforts such as Open‑X‑Embodiment, NVIDIA GR00T, or Amazon Vulcan. However, China is increasingly producing approaches that are equivalent — and in some cases complementary — along the same trajectory toward “physical intelligence.”

The differentiator is less about a fundamentally different stack, and more about the consistent combination of large-scale embodiment datasets, end-to-end vision-language-action (VLA) models, and the systematic coupling of high-level planning with robust, contact-rich execution. These are precisely the building blocks that separate a compelling demo from a reliable deployment.

The Quanta robot is intended to provide a path to humanoids in the household. Source: X Square Robot

Technology is leaving the lab — pilots must deliver economic value

For humanoid robots and physical AI in China, we expect a shift in 2026 away from headline-grabbing spectacles and toward real applications with commercial value. Investors are demanding it.

The anticipated IPO of Unitree in 2026 could become one of the larger Chinese robotics tech listings in some time, with more likely to follow. At the same time, consolidation will accelerate as weaker players fall away.

While U.S. companies such as Physical Intelligence, Skild.ai, and Google Gemini Robotics still lead on generalization, Chinese providers like X Square, TARS, AgiBot, Galaxea, and Galbot could benefit from offering full-stack systems built around clearly defined tasks. This enables faster iteration cycles, higher reliability, and better cost/performance — because every component is optimized as part of a tightly integrated system.

High-quality, real-world data is fuel

Chinese companies are also leaning harder into real-world operational data to improve their models.

On Dec. 30, 2025, the startup TARS Robotics — founded about 11 months earlier — released its open “World in Your Hands” dataset. Similar to the autonomous driving playbook, the company argues that high-quality, human-centric data is the critical fuel for physical AI.

According to TARS, its data collection approach can generate up to 1.8 TB per operator, per day of high-precision 6D motion data. The company says this helped raise robot success rates on complex manipulation tasks in unstructured environments from about 8% to about 60%.

Chinese robotics startups have raised significant funding in the past few years. Source: STM Stieler

Openness and network effects as a Chinese platform strategy

On Jan. 4, Galaxea Dynamics introduced its G0 Plus with an out-of-the-box VLA model. The company now ships its mobile dual-arm robots with a pre-installed, openly available VLA.

In the “Pick Up Anything” demo, it showed a full pipeline — understanding natural language, planning actions, and executing in the real world — including zero-shot capability.

The system was trained on the Galaxea Open-world Dataset (GOD), which includes real-world data from classic grasping tasks as well as more complex interactions. The company said its plug-and-play approach enables developers to get the system running in under 30 minutes and then fine-tune it for new tasks.

This strategic positioning could help Galaxea build a platform role in AI-enabled robot control over the medium to long term.

Hybrid form factors matter more for ROI calculations

Intralogistics use cases — alongside simple assembly and inspection tasks — are among the first applications that Chinese makers of humanoids aim to commercialize in 2026.

Notably, the Chinese companies with the strongest AI models for two-arm manipulation tend to be pragmatic about the humanoid form factor: All of them also have wheeled robots in their portfolios.

In parallel, industrial robots will increasingly benefit from advances in VLA models — and there is meaningful overlap with humanoid robotics. For example, AgiBot demonstrated a system at an electronics manufacturer in November in which robot changeover time was reduced to an average of 10 minutes using a combination of teleoperation and reinforcement learning.

Although AgiBot is among the best-funded Chinese startups in physical AI and also builds its own humanoid robots, the pilot used robot arms from Franka Robotics (formerly Franka Emika).

About the author

About the author

Georg Stieler advises some of the world’s largest robotics companies. He spent more than 10 years living in China and now splits his time between Switzerland and the People’s Republic of China.

Thanks to multi‑year, close collaboration with AI startups in Silicon Valley, Stieler is also deeply familiar with its culture.

The post Chinese robotics outlook for 2026 includes cobot growth, competitive pressure appeared first on The Robot Report.

View Source